The LED Lighting - LEED Building Tax Advantage

The LED Lighting LEED Building Tax Advantage:

LED lighting is being rapidly introduced into leading buildings. LEED certification is the widely renown marquee standard for recognizing sustainable buildings and has become an essential criteria for claiming Class A office building status.

There are now approximately 6,000 LEED buildings in the United States with 19,000 buildings currently going through the U.S. LEED certification process. LEED buildings have a distinct tax advantage in that due to their already documented energy reduction achievements many LEED buildings will qualify for a $1.80 EPAct tax deduction with the right LED lighting designs. Although they are energy efficient and environmentally sustainable, most LEED certified buildings do not currently incorporate LED lighting when reducing energy consumption. This article explains how to identify and capture large LED lighting EPAct tax deductions.

Standard EPAct definition:

Pursuant to Energy Policy Act (EPAct) Section 179D, building owners making qualifying energy-reducing investments in their new or existing building locations can obtain immediate tax deductions of up to $1.80 per square foot.

If the building project doesn't qualify for the maximum $1.80 per square foot immediate tax deduction, there are tax deductions of up to $0.60 per square foot for each of the three major building subsystems: lighting, HVAC (heating, ventilating, and air conditioning), and the building envelope. The building envelope is every item on the building’s exterior perimeter that touches the outside world including roof, walls, insulation, doors, windows and foundation.

LED Lighting Defined

Commercial building facilities managers, financial executives and tax departments are beginning to encounter the first stages of the inevitable widespread introduction of light emitting diode (LED) lighting for building interiors . These intriguing semiconductor devices produce powerful amounts of energy-efficient light with a much longer life cycle than current generation lighting products. Despite current high purchase costs for certain first mover applications; this method of lighting can result in substantially lower operating costs.

To consumers, the most familiar direct analogy to the fast-changing LED market is the replacement of incandescent bulbs by compact fluorescent (CFCs). When CFCs were first introduced, prices were very high, and despite the much longer life cycle, consumer acceptance was slow. Today, the benefits of CFCs are widely accepted and have assumed the most prominent position on home improvement and hardware store shelves.

Most of us are now familiar with a wide range of special purpose LED applications, including traffic lights, exit signs, automobile tail lights and stage lighting. Now LED lighting is quickly mainstreaming into building interior applications. Property owners have three years remaining until December 31, 2013 in order to monetize their LED lighting EPAct tax deductions .

LEED Defined

LEED, which stands for Leadership in Energy and Environmental Design, is the fast growing marquee standard for sustainable buildings. LEED is the certification system established by U.S. Green Building Council (USGBC). The four certification achievements start at the LEED certified level and proceed to the higher LEED silver, gold, and platinum levels .

The Best LEED Building Large LED Lighting Tax Deduction Candidates

Non Conditioned LEED Buildings:

Heating Non Conditioned Buildings meaning non air conditioned buildings are typically very good $1.80 LED tax deduction candidates.

The most common examples of non conditioned buildings are warehouses , manufacturing facilities , self storage centers , and the service areas of car dealerships .

The mathematical reason for this is that in non air conditioned spaces lighting makes up the largest portion of energy cost. Accordingly a large reduction in lighting energy usage in non conditioned spaces is much more likely to result in the 50% overall energy cost reduction required for the $1.80 cost tax deduction.

Conditioned LEED Buildings:

In conditioned LEED buildings, meaning cooled buildings, air conditioning is the biggest building energy user. Conditioned LEED buildings will qualify for the $1.80 LED lighting tax deduction when the buildings HVAC system is very energy efficient.

The best building candidates for this opportunity will be buildings with the following types of of HVAC: geothermal , thermal storage , energy recovery ventilation, magnetic bearing chillers , gas electric hybrid chillers10, and chilled beam technology.

•All buildings less than 150,000 square feet with chillers are good candidates

•Hotels and apartment building with chillers are also good candidates

To qualify for the $1.80 LED lighting tax deduction the building must be modeled in IRS approved software. Building owners should utilize tax engineers who are intimately familiar with the EPAct building modeling process. An experienced tax engineer will be able to confirm

before the LED LEED building lighting installation whether it is likely to qualify for the $1.80 LED lighting tax deduction.

Federal Government Moves to LEED Gold Standard

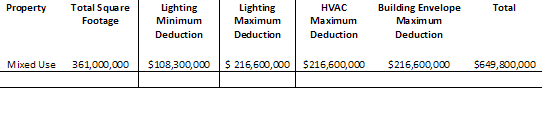

On October 28th, 2010 the GSA (General Services Administration) raised the standard for all new Federal government buildings and substantial building renovations to LEED Gold. This is an important development with major tax ramifications since the GSA has a portfolio of 9,600 owned or leased buildings totaling 361 million square feet.

With government owned or leased space the Section 179 EPAct LED lighting tax incentives go to the designer or design team members that effectuate the energy efficient LED design. Eligible design team members include but are not limited to architects, engineers, design and build contractors, lighting designers and ESCO's. The potential EPAct designer tax deduction for 361 million square feet are illustrated below:

GSA Potential LED/LEED Building Designer

EPAct Lighting Tax Deductions

Conclusion

LED building lighting has the advantage of a much longer useful life and the accompanying maintenance cost reductions, however it is currently expensive. The opportunity to increase a $.60 lighting EPAct tax deduction to a $1.80 whole building energy cost EPAct tax deduction makes LED lighting much more economically viable. LEED buildings can use their existing building energy simulation models to quickly make the determinate if there is eligibility for the $1.80 maximum deduction.

Sources

Goulding, Charles, Goldman, Jacob, & Goulding, Taylor. “The Economic, Business and Tax Aspects of Light Emitting Diode Interior Building Lighting” Corporate Business Taxation Monthly. January 2009. Pg 31-32.

Goulding, Charles, Goulding, Taylor, & Aboff, Amelia. “How LEED 2009 Expands EPAct Tax Savings Opportunities” Corporate Business Taxation Monthly. September 2009. Pg 11-13.

Goulding, Charles, Wood, Kenneth, & Kumar, Raymond. “Optimizing the 3, 2, 1 LED Lighting Tax Deduction Countdown” Corporate Business Taxation Monthly. July 2010. Pg 13-14, 47-48.

Goulding, Charles, Goldman, Jacob, & Most, Joseph. “Complete Warehouse Tax-Enhanced Energy-Efficient Design” Corporate Business Taxation Monthly. August 2010. Pg 17-19.

Goulding, Charles, Audette, Daniel, & Marr, Spencer. “The EPAct Tax Aspects of Resurging U.S. Manufacturing Investments” To be published in Corporate Business Taxation Monthly.

Goulding, Charles, Kumar, Raymond, & Goulding, Taylor. “Energy and Tax Savings Opportunities for Self-Storage Facilities” Corporate Business Taxation Monthly. September 2010. Pg 13-14, 40-41.

Goulding, Charles, Goldman, Jacob, & Kumar, Raymond. “Energy Tax Aspects of Car Dealerships” Corporate Business Taxation Monthly. July 2009. Pg 11-12, 45-46.

Goulding, Charles, Most, Joseph, & Marr, Spencer. “Energy Tax Aspects of Geothermal Heat Pumps” Corporate Business Taxation Monthly. December 2010. Pg 13-11, 36-37.