Record Hot Summer Puts Emphasis on AC Tax Opportunities

Record Hot Summer Puts Emphasis on Air Conditioning Tax Opportunities

Coming off a record hot 2010 summer at the peak of the economic downturn, many property owners are now focused on upgrading their air conditioning systems. There are multiple tax opportunities for replacing air conditioning which have been further enhanced by the December 2010 tax bill extension. Because the air conditioning equipment and controls industry is dominated by huge multi-industry manufacturers with multiple product lines who primarily sell through very small HVAC contractors, the tax and other incentive opportunities are rarely communicated to the end user purchasers. HVAC (Heating, Ventilation and Air Conditioning) replacements generally require large investments. This article is intended to help both manufacturers and end users better understand their tax opportunities and hopefully help both parties step up better equipment.

The Industry

Optimal air conditioning performance and efficiency comes from combining the right equipment for a particular building type and size, and operating the equipment with an appropriate HVAC controls system.

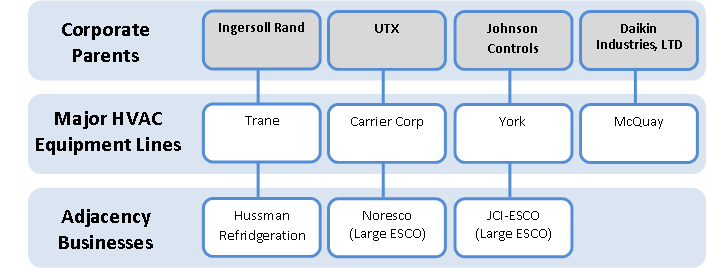

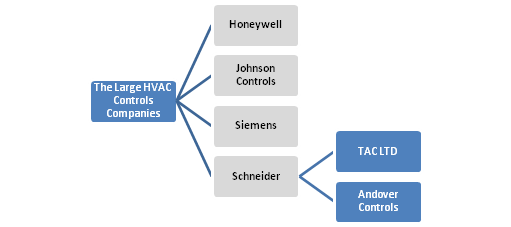

The U.S. air conditioning industry is dominated by four major equipment manufacturers and four HVAC controls companies, all of which are owned by some of the world’s largest corporations. The ownership structure, including corporate parent for these 8 manufacturers, is presented in the diagram below:

HVAC Industry Diagrams

The Big Four Equipment Manufacturers

The Big Control Companies

The Tax Opportunities

Pursuant to Energy Policy Act (EPAct) Section 179D, buildings making qualifying energy-reducing investments in their new or existing locations can obtain immediate tax deductions of up to $1.80 per square foot.

If the building project doesn't qualify for the maximum $1.80 per square foot immediate tax deduction, there are tax deductions of up to $0.60 per square foot for each of the three major building subsystems: lighting, HVAC (heating, ventilating, and air conditioning), and the building envelope. The building envelope is every item on the building’s exterior perimeter that touches the outside world including roof, walls, insulation, doors, windows and foundation.

Tax Credits/Cash Grants/Bonus Depreciation

IRS Sec 48 provides for a 10% tax credit for geothermal heat pumps used for building cooling if the customer installs them before December 31st 2017 .

In lieu of the 10% tax credit, geothermal heat pumps are also eligible for an equivalent 10% cash grant if the customer installs the heat pumps between January 1st 2009 and December 31st 2011. The December 2010 tax bill provides for 100% bonus depreciation for eligible alternative energy items, including geothermal.

The Importance of Building Size, Building Type and Energy Consumption

It is critically important to realize that the building size, building type and amount of energy consumption determines not only the choice of air conditioning equipment, but directly impacts the tax treatment.

Building Size

The EPAct tax provisions use an ASHRAE (American Society of Heating, Refrigerating and Air-Conditioning Engineers) building definition where there are three different size rules:

(1)Less than 75,000 sq ft

(2)Less than 150,000 sq ft, and

(3)150,000 sq ft or greater

There are two major categories of standard air conditioning systems for buildings, either package units or chillers. In general, package units are used in smaller buildings and more energy efficient chillers are used in larger buildings (particularly buildings 150,000 sq ft or greater).

Buildings less than 75,000 sq ft

Here, a package unit without VAV (Volume Air Ventilation) is the ASHRAE reference building energy savings is measured against. This means that any time VAV and/or a chiller or even more energy efficient equipment is installed, EPAct tax savings is probable.

Buildings less than 150,000 sq ft

Here, a package unit is the ASHRAE reference building equipment that energy savings is measured against. This means that any time a chiller or even a more efficient technology is installed, an EPAct tax deduction is probable.

Buildings 150,000 sq ft or great

er

Here, since the ASHRAE reference building model presumes a more efficient conditioning system. Since, by definition, these buildings confront very high energy costs, to maximize energy efficiency and EPAct tax benefits, a designer should consider selecting a very efficient HVAC technology. Examples of the different HVAC concepts and their efficiency can be found later in this article.

Building Types

EPAct air conditioning tax savings is only available for commercial buildings using an ASHRAE definition. The two major building categories under ASHRAE and hence the EPAct are commercial and residential. A residential building must be a rental apartment building and four stories or above to qualify for EPAct. This is because, for ASHRAE purposes, a rental property four stories or above is considered a commercial building. The ASHRAE reference comparison for residential buildings is for less efficient individual room units. An EPA tax act deduction is probable anytime an owner uses a central system including a chiller with a residential building four stories or above.

Commercial buildings get the best of all worlds in terms of EPAct treatment. Hotels and motels are considered commercial buildings, so all are eligible for EPAct regardless of the number of floors. Additionally, like residential buildings, they benefit from the more favorable HVAC individual room unit comparison. This means that anytime a hotel uses a central HVAC system, EPAct tax deduction is probable .

Energy Use

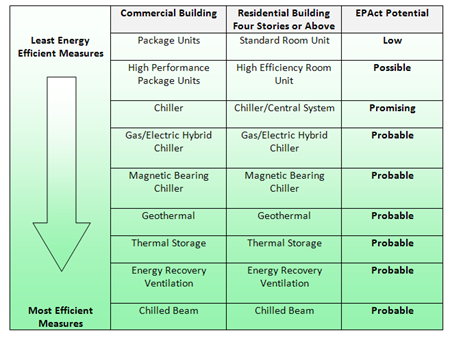

Large buildings, refrigerated buildings, campuses, supermarkets and complexes that use a lot of energy get the added economic leverage from using more expensive but much more energy efficient special HVAC measures including high performance chillers , geothermal , thermal storage , energy recovery ventilation and chilled beam technology.

Air Conditioning/HVAC EPAct Checklist

The following chart is designed to put all of these building and Air Conditioning/ HVAC concepts into one easy tax focused reference checklist.

HVAC Energy Efficiency Continuum

EPAct Tax Deduction Potential

Air Conditioning (HVAC) Controls

Since air conditioning and HVAC systems are the largest energy users in conditioned buildings, optimizing the use of these systems can greatly reduce operating costs. The first step should be to install the highest energy efficiency level of air conditioning equipment and the second step should be to control it. HVAC systems have numerous energy consuming components so the more equipment subject to control, the more costs savings. HVAC energy control systems have similar attributes to residential thermostats. Items that can be controlled include temperature ranges, hours of operation, number of occupants (based on CO2 levels), air changeover and heat transfer balancing outside air intake and inside air exhaust and optimizing the hourly integration of the different building systems. Improvements in software and wireless systems have made it more cost effective to bring more HVAC system components under control by the HVAC control system

Utility Rebates

Since air conditioning is generally the biggest building energy user in most buildings, large utility rebates are offered in many jurisdictions particularly for high performance air conditioning measures.

It is important to investigate utility rebates before ordering product since many HVAC utility rebates, particularly for high performance measures, require pre approvals.

Conclusion

Air conditioning is the largest building equipment energy user in conditioned buildings. Informed tax advisers can help building owners use tax savings to greatly reduce their building operating costs and after tax investments costs related to the existing system upgrades.

References

Goulding, Charles, Joseph Most & Spencer Marr. “Energy Tax Aspects of Geothermal Heat Pumps” Corporate Business Taxation Monthly. December 2010. Pg 13-11, 36-37.

Goulding, Charles, Jacob Goldman & Raymond Kumar. “Advanced EPAct Tax Planning for Hotel Chains” Corporate Business Taxation Monthly. June 2010. Pg 13-14, 36-37.

Goulding, Charles, Jacob Goldman & Joseph Most. “Energy Tax Aspects of Chillers” Corporate Business Taxation Monthly. October 2010. Pg 15-16, 41-42.

Goulding, Charles, Joseph Most & Spencer Marr. “Energy Tax Aspects of Geothermal Heat Pumps” Corporate Business Taxation Monthly. December 2010. Pg 13-11, 36-37.

Goulding, Charles, Jacob Goldman & Taylor Goulding. “The Tax Aspects of Thermal Storage and Time-of-Day Pricing” Corporate Business Taxation Monthly. November 2009. Pg 13-14, 37-38.