Utility Tax Planning for Coal Power Plant Closures

Utility Tax Planning for Coal Power Plant Closures

On December 2nd, 2011 the EPA moved ahead with rules requiring deep cuts in power plant emissions related to mercury, acid gases and soot derived from coal-fired utility plants over the next three years. Utilities impacted by these rules confront a decision analysis challenge that requires dynamic modeling and sensitivity analysis often involving tax implications. Utilities essentially have eight business planning options that can be used concurrently to address non-complying plants. The options are: 1. Close non-complying plants; 2. Replace existing plants; 3. Retrofit existing plants; 4. Change to clean fuel sources; 5. Seek a 4-year reliability phase-in; 6. Substantially reduce energy demand; 7. Accelerate alternative energy investments; 8. Implement curative corporate mergers.

The Section 179D EPAct Tax Opportunities

Pursuant to Section 179D of EPAct and its underlying ASHRAE (American Society of Heating Refrigeration and Air Conditioning) building energy code, commercial buildings including utility power plants are eligible for energy efficiency tax deductions of up to $1.80 per square foot. If a building’s energy reducing investment doesn’t qualify for the full $1.80 per square foot deduction, then deductions are available for any of the three major sub-systems, including:

1. Lighting

2. HVAC (Heating, Ventilation and Air Conditioning).

3. The building envelope.

Each component can qualify for up to 60 cents per square foot in EPAct tax deductions. The building envelope is anything on the perimeter of the building that touches the outside world including roof, walls, windows, doors, the foundation and related insulation layers.

Alternative Energy Tax Credits & Grants

There are multiple 30% or 10% tax credits available for a variety of alternative energy measures with varying credit termination dates. For example, the 30% solar tax credit and 30% fuel cell credit expires January 1st 2017 and the 10% Combined Power tax credit also expires January 1st, 2014. The 30% closed loop and open loop biomass credit expires January 1st, 2014.

All alternative measures that are eligible for the 30% and 10% tax credits are also eligible for equivalent cash grants for the three years staring January 1st 2009 and ending December 31st 2011.

The New Emissions Rules

The EPA’s new rule would call for extensive cuts in emissions of mercury, acid gases and soot from coal-fired power plants by setting maximum emissions levels allowed by utility plants. The law requires power plants to put in place proven and widely available pollution control technologies . In order to meet these emission reduction requirements, our view is that utilities will have 8 options:

1. Close Non-Complying Plants

Many of the plants scheduled for closing are small, older facilities where the cost of compliance would exceed the cost of replacing plants. Moreover, some of the older plants are substantially underutilized and can easily be taken off line by reducing demand (see section 5 and 6 below). It is estimated that at least 51 plants will be closed. Plant closures often have a major negative impact on local real property and personal property tax revenues.

2. Replace Existing Plants

The new rules are 22 years in the making, so utilities have had plenty of time to bring new replacement plants on line. In fact, 60% of the nation’s 1,400 affected coal and oil fired plants already comply with the new rules. Perhaps unsurprisingly, some major utilities, including Exellon and Calpine, support the new rules because they rely less on coal burning generation.

3. Retrofit Existing Plants

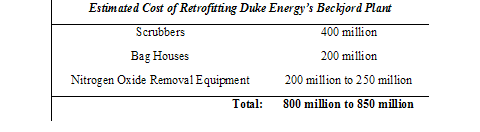

The retrofit of existing plants presents complex capital expenditure planning analysis since the cost to retrofit can easily range from hundreds of millions of dollars per facility to a billion dollars or more. For example, Duke energy estimated that the cost of retrofitting its Beckjord, Cincinnati plant would exceed 800 million dollars as follows:

These costs far exceed the costs of building a new gas-fired power plant at $500 to $750 million.

4. Change Fuel Sources

It is essentially the processing of fossil fuels, particularly coal, that is causing the non-compliant emissions. One solution that may be feasible in certain situations is a power plant fuel source conversion to a clean fuel such as biomass or solar thermal. Most clean fuels are potentially eligible for large alternative energy tax credits.

5. Four-Year Reliability Phase In.

Here, states that will enforce the standards are encouraged to allow utilities a four-year window in which they can comply "when justified," meaning that the utility must prove to the state that there is a good cause for their delay.

Hopefully the states will exercise this discretion when a utility demonstrates that it is making a major effort to reduce demand and convert to alternative energy as discussed below.

6. Demand Management

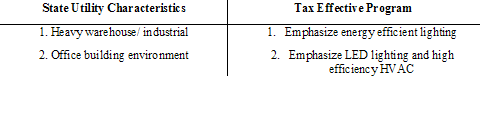

As a general rule, most of the utilities that provide low-cost coal-generated electricity have done little to encourage energy conservation. This means that in these jurisdictions, including for example Ohio and Virginia, there is a tremendous opportunity to reduce energy demand and in particular building energy demand where substantial Section 179D energy tax incentives are available. This means that tax departments serving the major coal burning utilities including AEP, Duke Power and the Southern company have an opportunity to assist in their companies’ avoidance of large capital expenditures by helping their organizations communicate the tax incentives to their commercial ratepayers.

To assist their utilities in reducing demand, tax departments need to understand that 1) lighting is the biggest energy user with non-air conditioned buildings and 2) air conditioning is the biggest energy user in buildings that do have air conditioning systems. Accordingly, utilities should structure their tax effective demand reduction programs as follows:

State Utility CharacteristicsTax Effective Program

Utilities with a need to substantially reduce overall energy use should target large energy users including manufacturers, cold storage facilities, supermarkets, hospitals, data centers and large office buildings

7. Accelerate Alternative Energy Investments

Many utilities have renewable energy commitments that require them to convert meaningful percentages of electricity demand in their jurisdictions to alternative energy. For instance, the federal EPA has issued guidelines for states regarding their Renewable Portfolio Standards (RPS) and 33 states either already have an RPS in place or have plans for adopting and RPS in the near future . Each state’s RPS varies, but they tend to require utilities to generate anywhere from 10%-30% of their power using renewable sources by 2025 at the latest. Since the new EPA emissions reduction requirements are applicable in the next three to four years and most of the large tax incentives for renewable energy expire on January 1, 2017, one strategy is to increase alternative energy projects and use these accomplishments to simultaneously meet multiple goals. For example, New Jersey has implemented an aggressive solar P.V. program that now generates 500 megawatts of electricity annually.

8. Mergers

Utilities that are undercapitalized or lack the overall resources to address new EPA rules may find it makes sense to merge with a utility that has the resources. In fact one of the stated reasons for the large Duke/Progress energy merger was the expectation of more demanding emissions rules .

Basic utility emissions merger planning can be illustrated with the following example:

Assume a small utility (Small Power) has two power plants. Plant 1 is a small non-compliant plant operating at 35% capacity requiring $400 million in new investment to become compliant. Plant Two is compliant and operating at 80% of capacity. Small Power cannot close Plant 1 and remain a reliable power supplier solely relying on Plant 2.

Also assume that a large utility (Large Power) has multiple large plants that are compliant and operating at 70 percent of capacity. Further assume that Large Power is desirous of expanding into Small Power’s market.

Rather than investing $400 million in Plant 1 it may make sense for Small Power to merge with Large Power and simply close Plant 1 and actually improve reliability to its customers.

State Emission Reduction Rules

California and Massachusetts already have comprehensive emission reduction requirements. Tennessee has already acted to address the coal fuel source to non coal conversions process .

All three of these states have been leaders in energy efficiency and alternative energy programs and serve as good role models and sounding boards for the coal plant utility jurisdictions who are now considering implementing similar conservation and alternative energy programs as part of their overall business strategy.

Conclusion

Many utilities are currently analyzing the new EPA emissions rules. Non compliant utilities have variety of strategies to choose from and multiple strategies may be appropriate. With careful planning it may be possible to either avoid some large capital investments or improve the economic return on capital investments using tax planning.

References

http://www.epa.gov/chp/state-policy/renewable_fs.html

http://www.reuters.com/article/2011/12/15/us-dukeenergy-progressenergy-idUSTRE7BE14020111215