Using Underlying Building Characteristics to Pay for Roof Improvements

Property owners with large roofs particularly in the warehouse, industrial and self storage area have a unique opportunity to obtain large tax incentives for major roof improvements and roof repairs. For many existing buildings roofs are the most expensive items requiring end of life cycle replacement. This article explains how to use the commercial building Section 179D tax incentive and energy efficient lighting to plan into a large roof tax incentive.

The EPAct Tax Opportunity

Pursuant to Energy Policy Act (EPAct) Section 179D, warehouse owners or tenants making qualifying energy-reducing investments can obtain immediate tax deductions of up to $1.80 per square foot.

If the building project doesn't qualify for the maximum $1.80 per square foot immediate tax deduction, there are tax deductions of up to 60 cents per square foot for each of the three major building subsystems: lighting, HVAC and the building envelope. The building envelope is every item on the building’s exterior perimeter that touches the outside world including roof, walls, insulation, doors, windows and foundation.

Understanding the Lighting Tax Calculation that drives the $1.80 per square ft.

Warehouses that combine energy efficient lighting and heating have become by far the largest category of buildings qualifying for the $1.20 to $1.80 EPAct tax deductions. Most warehouses, industrial and self storage buildings are non conditioned meaning they are not air conditioned1.

Many existing warehouses, manufacturing facilities and self storage facilities have prior generation metal halide and or T-12 lighting, that is now federally banned, and needs to be replaced.

In non conditioned buildings lighting is by far the biggest building energy user. Section 179D requires a 50% overall building energy cost reduction and energy efficient lighting can achieve 42% and greater energy cost reduction alone. The remaining difference to achieve the 50% cost reduction can usually be achieved by a reasonably energy efficient heater.

Roof Tax Planning

Commercial Roof replacement is very expensive and can cost upwards of $4.00 per square ft. This means that with buildings 250,000 square ft and above roof replacement can easily exceed $1,000,000. The ability to take a large portion of roof capital outlay and convert it from a 39 year asset to an immediate tax deduction has tremendous economic value. Roofs require replacement when they are worn and often need to be replaced or improved in preparation for solar.

Tax Planning Examples

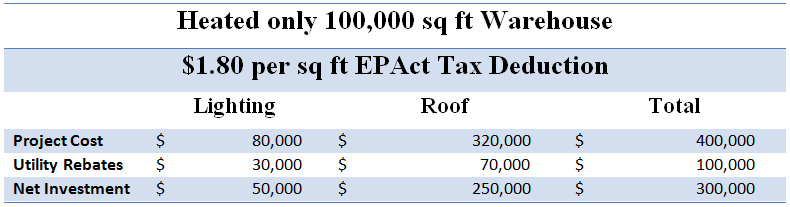

EPAct Qualifying 100,000 sq ft Warehouse Example:

If light power density is reduced to .45 watts/sq ft or less then the above example would achieve a $1.80/sq ft EPAct Tax Deduction in addition to the estimated rebates listed. At 100,000 sq ft, in this example having achieved maximum tax deduction the warehouse would receive a $180,000 EPAct tax deduction, worth $63,000 in federal tax saved, using a 35% federal tax rate.

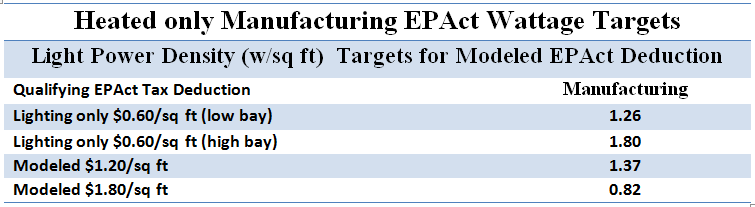

250,000 sq ft heated only Manufacturing Facility Example:

The lighting targets for manufacturing to achieve both lighting only and modeled tax deductions under EPAct are even easier to achieve in this building category than they are in a pure pick and pack warehouse. The targets represented below if achieved could generate a $450,000 EPAct Tax deduction.

Most times the project costs associated with achieving the wattage targets above and installing or replacing unit heaters, costs around $1/sq ft. In the case of the above Manufacturing facility if it were able to reduce its lighting watts/sq ft to .82, then the facility would fully qualify for $1.80/sq ft. Achieving the $1.80/sq foot would leave $0.80/sq ft or $200,000, in EPAct tax deduction, left over to apply to an envelope improvement, in this case a roof enhancement or replacement.

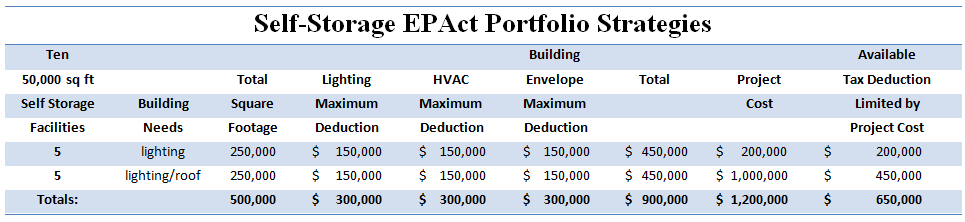

Self-Storage EPAct Portfolio Example:

The above chart indicates the strategy related to this tax deduction with regards to a portfolio. We have used the example of self storage as they are usually chains and have multiple locations. In this example there are 10 total facilities 5 of which need lighting retrofits and the other 5 which need lighting retrofits and roofs. The strategy in this case is to take advantage of the projects in which all of the deduction can be utilized. EPAct limits deductions to the lesser of the amount qualified for (by achieving certain energy benchmarks) or project cost, so the best projects have a high enough project cost to fully realize the deduction qualified for. In this case when retrofitting lighting in a heated only space, like these self-storage facilities, the project cost associated with only a lighting retrofit is likely only $0.80/sq ft, which leaves $1.00/sq ft left over. Lighting and the fact that the space is heated only, qualifies the space for $1.80, an additional spend on the envelope, raises the project cost above the $1.80 for which it has already qualified. This "left-over" $1/sq ft should be used to reduce the cost of the roof replacement/improvement.

Conclusion

The total project should take advantage of energy savings, rebates and tax savings to leverage all incentives. Knowing the EPAct targets ahead of time and making sure the internal systems qualify is important to achieve an EPAct Tax deduction. Planning ahead to take advantage of the largest tax deductions by reviewing portfolio needs is the best way to utilize EPAct to the fullest extent. Understanding all of these concepts and using them systematically will allow companies to take advantage of their underlying building systems to upgrade or replace roofs, a project with substantially higher costs than other building improvements.

1 - Charles Goulding, Jacob Goldman and Joseph Most, Complete Warehouse Tax Enhanced Energy Efficient Design, Corp. Bus. Tax'n Monthly, August 2010, at 17.

2 - Charles Goulding, Taylor Goulding, and Raymond Kumar, The EPAct Tax Aspects of Resurging U.S. Manufacturing Investments, Corp. Bus. Tax'n Monthly, June 2011, at 17.

3 - Charles Goulding, Taylor Goulding, and Raymond Kumar, Energy and Tax Savings Opportunities for Self Storage Facilities, Corp. Bus. Tax'n Monthly, September 2010, at 13.