Complete Warehouse Tax-Enhanced Energy-Efficient Design

Warehouses are becoming the break out category for tax enhanced energy efficient design. Warehouses are taking the lead in energy efficient design because they are large simple spaces where large energy and tax savings is easily achievable by installing current generation building products. Moreover the largest concentrations of large warehouses support nearby major population centers where electricity is often supply constrained and expensive which greatly increases the economic return from energy efficiency measures.

The EPAct Tax Opportunity

Pursuant to Energy Policy Act (EPAct) Section 179D, warehouse owners or tenants making qualifying energy-reducing investments can obtain immediate tax deductions of up to $1.80 per square foot.

If the building project doesn't qualify for the maximum $1.80 per square foot immediate tax deduction, there are tax deductions of up to 60 cents per square foot for each of the three major building subsystems: lighting, HVAC and the building envelope. The building envelope is every item on the building’s exterior perimeter that touches the outside world including roof, walls, insulation, doors, windows and foundation.

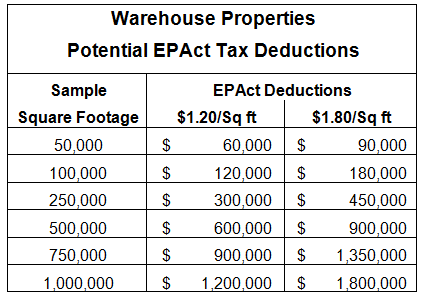

Warehouses that combine energy efficient lighting and heating have become by far the largest category of buildings qualifying for the $1.20 to $1.80 EPAct tax deductions. The following table illustrates the magnitude of potential EPAct tax benefits available at various square footage's:

Lighting

Building lighting comprises a large portion of warehouse energy use. Most warehouses that have not had a lighting upgrade to energy efficient lighting in the last 7 or 8 years utilize prior generation metal halide or T-12 fluorescent lighting. It is also important to realize that effective January 1, 2009 most probe-start metal halide lighting may no longer be manufactured or imported into the United States and effective July 1, 2010; most T-12 lighting may no longer be manufactured or imported into the United States. This means that warehouses that still have this lighting technology will soon be subject to large price increases for replacement lamps and bulbs.

This prior generation T12 and metal halide lighting is very energy inefficient compared to today's T-8 and T-5 lighting, and a lighting retrofit can easily reduce lighting electricity costs by 40 to 60 percent. In addition to large energy cost reduction from the base building lighting, most warehouses undergoing lighting retrofits install sensors that completely shut off the lighting in portions of the warehouse that are not in use. Previously, many warehouse owners and lighting specifiers were reluctant to install sensors because they reduced fluorescent lamp useful life. Today, improved technology sensors are available with warrantees not to reduce lamp useful life.

Heating

New, improved commercial heating systems can provide energy cost savings of eight percent or more over the ASHRAE 2001 building code standards. There are multiple heater technologies suitable for the warehouse market, including direct fired gas heaters, unit heaters, and infrared (radiant) heaters .

If feasible the warehouse heater should be mounted on an exterior wall to optimize the roof top solar P.V. space.

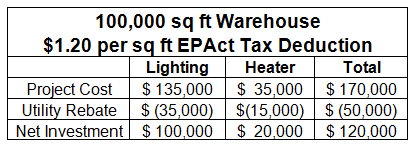

An example illustrating the maximum utilization of the $1.20 EPAct tax deduction for a 100,000 sq ft warehouse with an energy efficient heater is as follows:

With this example, the $120,000 (100,000 sq ft x $1.20) entire investment EPAct tax deduction will be achieved as long as the combined lighting heater project reduces total energy cost by 33 1/3% as compared to ASHRAE 2001.

Building Envelope

If a warehouse requires reroofing this owner should consider a more energy efficient white roof. Moreover, when reroofing this is the ideal time to consider adding more insulation. If the building already had an energy efficient design and roof the owner may want to consider upgrading to more energy efficient truck bay doors and windows.

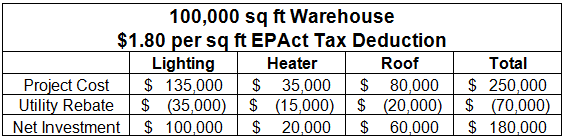

With this example the maximum $180,000 EPAct tax deduction (100,000 sq ft x $1.80) will be available as long as the combined lighting, heater and roof project reduces total energy cost by at least 50% as compared to ASHRAE 2001.

Solar P.V.

Solar P.V. rooftop systems are used to generate electricity at warehouses. Warehouses typically make ideal solar installation candidates since they often have large, unobstructed flat roofs. Large roofs enable large P.V. systems that generate more electricity. Solar P.V. installations are entitled to 30% tax credit or now for the first time a 30% grant . When using either the credit or the grant, five years MACRS deprecation is available. Often tax equity partners will be willing to make the investment for a rooftop warehouse solar installation and enter into a power purchase agreement where the warehouse operator post-installation will purchase its electricity at an agreed price for a fixed period of time, usually 15 to 20 years. The tax equity partner will use a combination of the power purchase agreement annual revenue, the tax credit or grant, utility rebates if available, green tag emission payments and net metering electricity payments for selling the excess power back to the grid to generate an acceptable economic return. With a power purchase agreement, a warehouse is essentially renting its roof as an alternate energy electrical generator.

Warehouse Tax Incentivized Energy Efficient Design Process Steps

1. Assemble team including Warehouse experts for EPAct tax incentives, utility rebates, lighting, heater, envelope and solar.

2. See if roof is compatible for solar and heater. Obtain solar and any needed roof/insulation proposals.

3. Obtain lighting design that replaces all inefficient lighting. Compare and contrast fluorescent, induction and LED lighting alternatives.

4. Obtain Cambridge heater or equivalent design proposal based on proposed roof design.

5. Determine utility rebate based on all proposed separate and combined measures. Lighting will reduce electrical use. Roof, insulation and heater will reduce therms.

6. Determine tax incentives including EPAct tax deduction benefit and solar credit tax deductions. EPAct will be based on total project square footage, including mezzanines and pick and pack modules. The 30% solar tax credit will be based on the combined solar material and installation costs.

7. Prepare project proposal integrating project cost, energy savings, utility rebates and tax incentives.

8. Get project approved.

9. Hire contractors and execute project.

10. Have EPAct modeler and tax expert prepare IRS approved software model and tax documentation.

11. Process utility rebates.

12. Reduce Federal and State estimated tax payments for large tax deductions and credits.

13. Celebrate tax enhanced energy efficient warehouse achievement.

Conclusion

As described above there are multiple compelling reasons including energy and substantial tax savings why warehouses are becoming the breakout energy efficiency project building category. This is such a widespread phenomenon that market forces will require warehouse landlords to upgrade just to remain competitive. Once the overwhelming majority of warehouses are upgraded America's building products community will undoubtedly turn their attention to the next major building category requiring improvement which may very well be the office building you are sitting in.

Charles Goulding, Attorney/CPA is the President of Energy Tax Savers, Inc., an interdisciplinary tax and engineering firm that specializes in the energy-efficient aspects of buildings.

Jacob Goldman, LEED AP, is and Engineer and Tax Consultant with Energy Tax Savers, Inc.

Joseph Most is an Analyst with Energy Tax Savers, Inc.

References

See Charles Goulding, Jacob Goldman and Taylor Goulding, Tax Planning for the 21st Solar Century, Corp. Bus. Tax’n Monthly, February 2009, at 23.

See Charles Goulding, Jacob Goldman and Raymond Kumar, Large EPAct Energy Tax Deduction Opportunities for Commercial Heaters, Corp. Bus. Tax’n Monthly, January 2010, at 11.