Manufacturing Facilities Drive Large EPAct Tax Deductions

Manufacturing Facilities Drive Large EPAct Tax Deductions

Manufacturing facilities present one of the best opportunities for large EPAct tax deductions. For EPAct purposes, a “manufacturing facility” is broadly defined to include a wide range of physical human activities including manufacturing, assembly, work shops, food processing, and repair. There are also varying types of environments presented in these facilities, such as dirty vs. clean, conditioned vs. non-conditioned , wet vs. dry, etc. The combination of these different conditions and spaces determine the appropriate energy efficient lighting fixtures and HVAC systems potentially eligible for EPAct tax incentives.

EPAct

EPAct (Energy Policy Act) provides an immediate tax deduction of up to $1.80 per square foot for building investments that achieve specified energy cost reductions beyond the American Society of Heating and Air-Conditioning Engineers (ASHRAE) 90.1-2001 building energy code standards. A one-time $1.80 per square foot deduction is the maximum tax deduction, but deductions of up to 60 cents per square foot are also available for three types of building systems: lighting, including lighting controls, HVAC, and the building envelope, which includes roof, walls, windows, doors and floor/foundation.

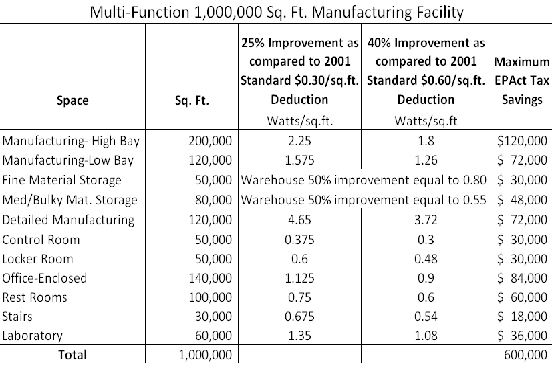

EPAct Lighting Tax Deductions for Typical Manufacturing Spaces

In a multi-function manufacturing plant illustrated in Figure 1 below, it is clear that the various spaces within the facility help generate large deductions. For a multi-function 1,000,000 square foot manufacturing facility to obtain a tax deduction of 30 cents per square foot for lighting, the wattage must be reduced by 25 percent from ASHRAE 90.1-2001 levels. A maximum EPAct lighting tax deduction of 60 cents per square foot requires a 40 percent reduction. For example, the 1,000,000 square foot manufacturing facility presented below can qualify for up to $600,000 in lighting EPAct tax deductions. The table included below presents the wattage targets for different categories of spaces found in manufacturing facilities.

Finding the Appropriate Lighting Fixture

Choosing the appropriate lighting fixture for a manufacturing facility depends upon the primary operation of the facility. It is important to note that specific areas within a facility may also require different lighting fixtures. Different stages within the assembly process may call for more or less lighting in order for workers to operate effectively. Office areas of the facility would not need the same fixtures as those in the central manufacturing area. Different fixtures are also required for refrigerated or freezer environments and dirty or oily environments. There is an excellent opportunity to qualify for EPAct lighting tax deductions because the manufacturing category ASHRAE lighting standards are the easiest to meet.

Federally Banned Fixtures

Many manufacturing facilities use prior generation lighting technologies: metal halide and T12 fluorescent fixtures. Metal halide fixtures are not recommended because they consume large amounts of energy and are very inefficient. As a result, most probe start metal halides have been federally banned from being manufactured as of January 1, 2009. T12 fixtures have also been banned due to their use of magnetic ballasts, effective since July 1, 2010.

T8 and T5 fluorescents lamps are smaller in size, more energy efficient, and last longer than T12 bulbs. By replacing T12s with T8s and T5s, a manufacturing facility is likely to qualify for the EPAct lighting tax deduction. 4

High-bay vs. Low-bay Fixtures

Traditional manufacturing plants commonly complete lighting upgrades using energy efficient high-bay or low-bay fluorescent fixtures. The difference between them is the height at which they are mounted. Low-bay fluorescents are those used in spaces that have a height of 20-feet or less while high-bay fluorescents are fixtures used in spaces with heights of greater than 20-feet. In manufacturing plants with heavy industrial production, high-bay fixtures are typically used. High-bay fluorescents are often used in wet, dirty, or oily environments. Since low-bay fixtures are mounted at lower heights, they produce a more concentrated beam of light that is useful in spaces where production areas must be well lit.

LED Lighting

As a result of very recent product development, there are now options to use LED fixtures which are more efficient than T8 and T5 fluorescent fixtures. LED (light emitting diode) lighting uses semiconductors called diodes to provide a lower energy consumption powerful light source. They last more than 50,000 hours, use less power, do not contain the hazardous mercury that fluorescents use, and typically qualify for the EPAct tax deduction. LEDs are particularly useful for task lighting, or equipment lighting, where manufacturing activities must be well-lit. These fixtures also start instantly at full brightness and operate at low temperatures, which is beneficial for refrigerated and freezer environments.

In manufacturing plants that produce large amounts of dirt, dust and oil, an LED fixture may not be the appropriate choice because dirt will reduce the amount of light produced. Fixtures may need to be cleaned and maintained regularly based on the amount of dirt and dust accumulation. While the initial costs for LEDs are high in comparison to traditional metal halides and T12s, in most cases the operating and maintenance costs often produce much greater savings. 6

Induction Lighting

Another lighting alternative that is increasingly popular is induction lighting. These fixtures are essentially fluorescent lighting without electrodes. Benefits to the use of induction lighting include a long life of over 100,000 hours, lower initial cost (compared to LEDs), and the ability to withstand cold temperatures and dirty environments. From a tax perspective, these fixtures usually qualify for the highest EPAct tax deduction because of their low wattage level. 4

Many factors weigh-in to finding the appropriate fixture; therefore the right fixture for one manufacturing facility may not be the right fixture for another manufacturing facility.

HVAC System EPAct Overview

Recent natural gas discoveries and major improvements in natural gas distribution in the US have promoted the development of highly energy efficient natural gas HVAC equipment. Like lighting, installing a very efficient HVAC system in a manufacturing facility can trigger large EPAct deductions. Manufacturing facilities are either conditioned, meaning the facility is air-conditioned, or non-conditioned meaning it is only heated. 7

Non-conditioned Facilities

Most manufacturing facilities are non-conditioned or non-air-conditioned heating-only buildings. In these facilities using an energy efficient heater is recommended to maximize the EPAct tax deduction. Recent major natural gas finds are encouraging building owners to switch to this fuel source. Cambridge Engineering direct fired units have been selected by the Environmental Protection Agency and Department of Energy as an energy partner to help save energy in industrial buildings. Lighting makes up the largest portion of manufacturing facility energy use. Accordingly, for non-conditioned spaces it is normally necessary to install energy efficient lighting before or concurrent with an energy efficient HVAC system to achieve an HVAC EPAct tax deduction. 5

Conditioned Manufacturing

In conditioned manufacturing facilities, one of the best technologies used for achieving substantial energy reduction and EPAct tax deductions is energy recovery ventilation (ERV). This technology uses the combination of a heat exchanger and ventilation system to heat or cool incoming fresh air, with the outflowing waste air, thereby recapturing 60 to 80 percent of the energy that would otherwise be lost. This technology is particularly useful for manufacturing processes that require controlled temperatures and humidity levels. Another alternative is geothermal heat pumps which use the transfer of heat from the earth to provide heating or cooling.

The use of energy efficient HVAC systems leads to large EPAct tax deductions. The HVAC system itself, particularly those using geothermal heat pumps, can qualify for an immediate 60 cents per square foot deduction or $1.80 per square foot for the entire building. In facilities 150,000 square feet or less with highly efficient systems, there is an even greater chance of qualifying for EPAct since the ASHRAE 2001 reference building, which is the building type it is compared to, uses less energy efficient HVAC systems. 8

Controlling Energy Consumption

Once an energy efficient HVAC system is installed there are other ways to achieve additional energy savings. For instance, using VFDs (variable frequency drives) minimizes the energy use of motors. Setting electronic on/off controls or occupancy sensors will turn off the system and ensure energy is not wasted during the facility’s off hours. To reduce energy consumption throughout the year, set weekend temperatures higher or lower during summer and winter seasons, respectively. 8

The LEED Advantage

Companies like General Motors and Starbucks are recognized for their LEED certified manufacturing facilities. The LEED (Leadership in Energy and Environmental Design) certification developed by the US Green Building Council (USGBC) is the recognition of buildings as energy efficient, or “green” in terms of design, construction, operation and maintenance. Earning a LEED certification for a manufacturing plant is a significant achievement according to the USGBC because industrial facilities typically produce large amounts of waste. LEED manufacturing plants present a great opportunity for EPAct tax deductions because they already have a building energy simulation model that can be converted into an EPAct tax model. Figure 2 highlights the potential tax savings available for a few LEED certified manufacturing plants. Figure 2.

Conclusion

Manufacturing facilities are ideal buildings for potential EPAct tax deductions. A manufacturing facility can further increase its ability to qualify for the EPAct tax deduction by improving energy efficiency in all spaces, choosing the proper fixture for each space, and installing a more efficient HVAC system or heater. Using these recommendations ensures that a manufacturing facility can improve its energy efficiency and generate large tax deductions and energy savings.

References

Bristol-myers squibb: An example of why project labor agreements are a sound business choice.http://builtbest.org/feature-story-sample

2 Energy star. (2010). http://www.energystar.gov/

3 GM opens first ever LEED gold certified plant.http://www.reliableplant.com/Read/2221/gm-opens-first-ever-leed-gold-certified-plant

4 Goulding, C., Goldman, J., & Kumar, R. EPAct aspects of induction lighting. To be Published by CCH, Inc: Corporate Business Taxation Monthly.

5Goulding, C., Goldman, J., & Kumar, R. Large EPAct energy tax deduction opportunities for commercial heaters. Corporate Business Taxation Monthly, (January 2010), 11-12, 28, 29.

6 Goulding, C., Goulding, T., & Kumar, R. (September 2009). LED parking garage lighting installations accelerate with EPAct tax savings. Corporate Business Taxation Monthly, 15-16, 46.

7 Goulding, C., Goulding, T., & Most, J. (to be published by CCH, Inc: Corporate Business Taxation Monthly). Abundant natural gas heats up large tax incentives for gas fueled building energy equipment.

8 Goulding, C., Kumar, R., & Wood, K. New efficient HVAC drives large tax deductions for buildings. Corporate Business Taxation Monthly, (May 2009)

9 Nestl� waters: Arrowhead plant, cabazon, california.http://www.nestle-watersna.com/Menu/Environmental/GreenBuildings/LEED/Cabazon.htm

10 Starbucks opens leed certified coffee roasting plant.http://news.starbucks.com/article_display.cfm?article_id=170